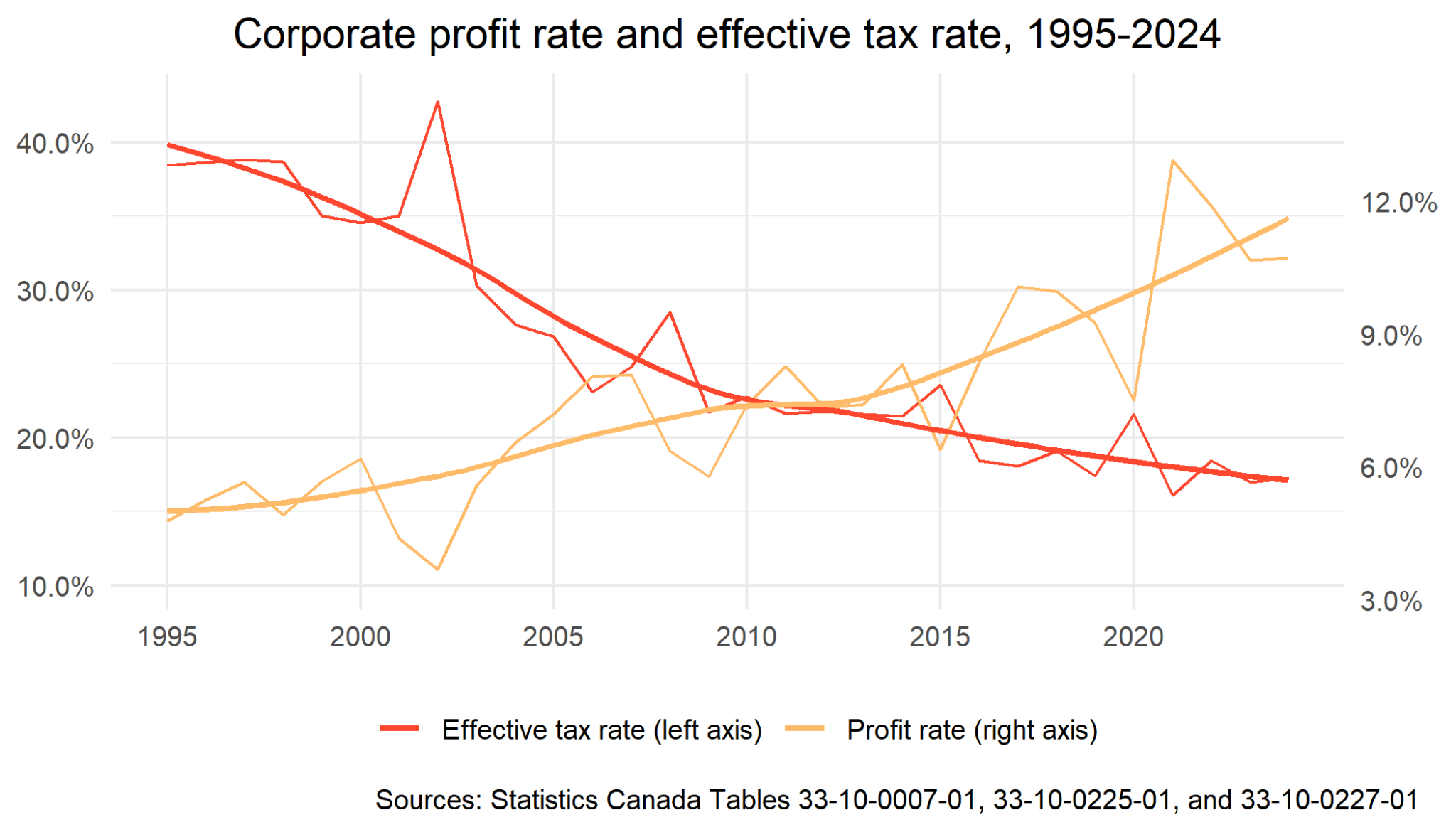

Few single figures capture the power of corporations as well as the corporate profit rate.1 This shows the proportion of every dollar collected by corporations that was not needed to pay workers or purchase equipment and materials. While variation in profit rates across firms and industries arises because of factors unique to each firm and industry, profit rates at the aggregate level are an excellent indicator of corporate power as a whole. Essentially, profit rates show the magnitude that corporations are able to set prices above their costs, accruing wealth for themselves and their shareholders, instead of paying it to workers.

So, how has corporate power changed in Canada over the past 30 years? In 1995, the corporate profit rate was 4.8%. In 2023, it had more than doubled to 10.7%. As shown in the chart below, these are not outlier years. On the contrary, they are part of a long-term trend of increasing corporate power in Canada. Outside of brief recessionary periods, the corporate profit rate has steadily increased, from 5% in the late 90s to 7-8% in the mid-2000s, to 9-10% in the late 2010s, and now to around 11% in the early 2020s. Although profit rates have fallen from their all-time high in 2022, the long-term trend (the thick yellow line in the figure below) shows profit rates are still on an upward trajectory and have not returned to pre-pandemic levels.

Graph of the corporate profit rate and effective tax rate, from 1995 to 2024, with the corporate profit rate steadily rising as the tax rate steadily falls. At the same level around 2011.

Notes: Profit rate is calculated as "Income or loss before income taxes" divided by "Total operating revenue". Effective tax rate is calculated as "Income tax" divided by "Income or loss before income taxes". From 2010 onwards, "Income tax" is replaced with "Income or loss before income taxes" minus "Income or loss after income taxes. 2024 data only includes the first two quarters. Thick lines are long-term trends calculated using local polynomial regression.

Over the same period, corporate tax rates have consistently been slashed. The general federal tax rate on corporate income was 29.12% in 1995 (already significantly lower than the 41% rate that applied in 1960), and has been lowered to 15% as of 2024. The decrease in the federal statutory corporate tax rate underestimates the real fall in corporate income taxation. This is because of the proliferation of deductions and exemptions. As shown in the figure above, the effective corporate tax rate, the percentage of profits actually paid in income taxes, fell from 38.4% in 1995 to 17% in 2023.

Rising corporate profits and falling corporate tax rates are related. Corporate tax cuts encourage higher profits by increasing the share of profits that shareholders get to keep. Proponents of cutting corporate taxes typically argue that it will promote investment and eventually lead to higher productivity. But, over the past 30 years, the opposite has happened. In the late 1990s, annual labour productivity growth was over 2%. Now, it is less than 1%.

In fact, while workers’ wages and tax revenue have stagnated, payouts to shareholders and corporate executive pay have skyrocketed, resulting in rising inequality and cuts to public services. International studies show that tax cuts for the rich increase inequality without leading to growth. We must stop buying the narrative that cutting corporate taxes makes everyone better off.

Rising corporate profits and lower corporate taxes are not inevitable. Instead, they are the result of a shift in power away from workers towards corporations, and of policy choices. Reversing these trends requires building worker power to win a fairer distribution of income and demanding policies that prevent corporate profiteering. Only then will we be able to build a more democratic economy and create fairness for all Canadians.

Take action on tax justice in Canada here.

1 Here, the corporate profit rate is defined as the total profits of corporations divided by their total operating revenue.