Despite Canada’s commitment to end subsidies for fossil fuel companies, Canada’s oil and gas (O&G) sector is still a top recipient of tax benefits from both the federal and provincial governments.

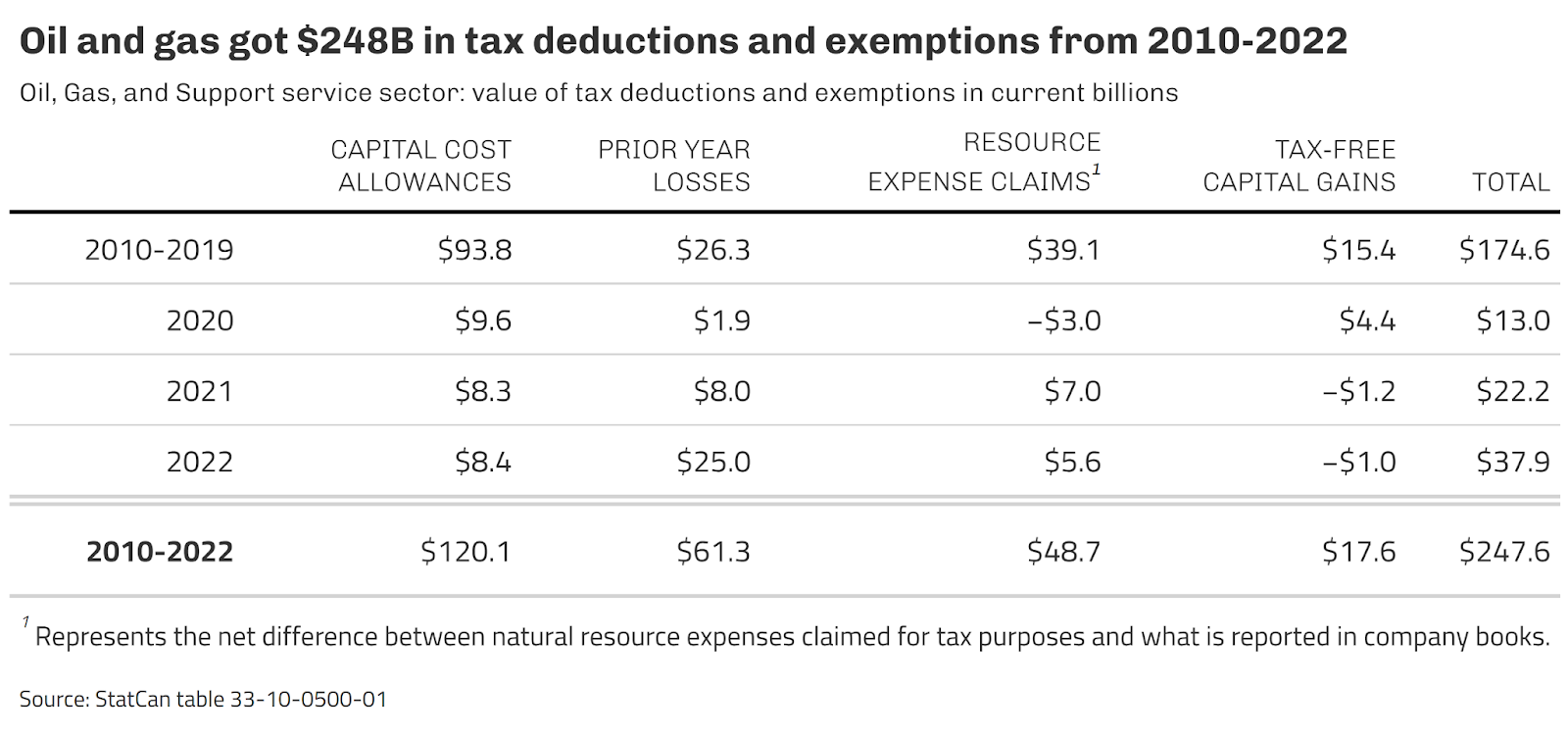

From 2010-22, O&G received nearly one-quarter trillion dollars ($248B) in income tax deductions from capital cost allowances (CCAs), natural resource expense claims, prior year losses applied, and capital gains exemptions. The sector received an additional $16.6B in refundable tax credits. During those years, O&G ranked first among non-financial industries in tax benefits received.

Capital cost allowances a key component of subsidizing fossil fuels

CCAs, a special tax deduction on the depreciation of certain capital investments, are the most important tax benefit for the O&G sector. While CCAs are available to all industries, O&G receives a disproportionate share of CCA deductions compared to their role in the economy. In fact, CCAs represent nearly half (48.5%) of the total income tax deductions and exemptions reported by O&G.

The numbers are clear: generous CCAs are supporting increased fossil fuel production

As CCAs are designed to encourage capital investment into productive assets, substantial investments into fossil fuel production have been supported by these tax benefits. About two-thirds of the sector’s capital spending since 2020 ($80B) went into depletable assets, which are investments in bringing oil and natural gas properties into production through exploration and development.

The government sometimes provides generous CCA rates, meaning the allowed deduction is larger than the depreciation, to encourage investment in certain sectors. In recent years, O&G has enjoyed the most generous CCA rates by far. From 2010-22, O&G enjoyed an excess CCA rate of 36%, while the excess rate for all non-fossil fuel industries was virtually zero. Overall, O&G companies accounted for 6.7% of all depreciation, yet nearly two-thirds (63%) of excess CCAs.

From the start of 2010 to the end of 2023, Canadian crude oil production more than doubled from 2.5 to 5.4 million barrels per day. Analysis by the International Energy Agency predicts that the opening of the TMX pipeline will spur strong production growth, leading to record-breaking oil production levels through 2030.

A lack of transparency on tax benefits flowing to the fossil fuel sector makes it difficult to determine why O&G receives such generous CCA rates compared to other industries. From 1999-2015, accelerated CCA rates were provided to O&G with the justification of incentivizing investments in emissions reduction. Despite this, no estimates for the value of these tax deductions were ever produced. Since 2018, O&G has taken advantage of accelerated rates offered through the Accelerated Investment Incentive (AII), which is set to be phased out from 2024 to 27. Insufficient data prevents us from knowing the value of O&G deductions made under the AII.

Recommendations from Canadians for Tax Fairness

- Consider all forms of tax benefits for the fossil fuel sector as part of Canada’s pledge to eliminate public subsidies and financing of fossil fuels.

- Ensure that generous CCA rates do not undermine Canada’s climate commitments by incentivizing expanded fossil fuel production.

- Increase transparency around tax benefits going to the fossil fuel sector.

Continued subsidization of fossil fuel production contradicts Canada’s commitment to climate action. With wildfires raging across the country each summer, the urgency to stop environmental destruction from fossil fuels has never been greater. Ending tax breaks to the O&G sector is an important place to start.

Take action to end Canada's tax support for O&G here.